How Honeywell’s Data Center Power Management Collaboration Is Shaping Its Investment Story

A Strategic Partnership for Smarter Energy

Honeywell joined forces with LS Electric to transform data center power management.

The two companies now build integrated hardware and software to simplify complex energy operations.

They aim to help data centers and building operators run smarter, faster, and more reliably.

This move also strengthens Honeywell’s reach across the global digital infrastructure ecosystem.

Expanding Honeywell’s Role in Critical Infrastructure

Honeywell wants to become a one-stop supplier for both building automation and power systems.

By combining controls and energy management, it targets higher efficiency and resilience for operators.

The data center boom gives Honeywell a clear runway for growth in automation and power solutions.

This integration shows how the company adapts to modern energy demands while expanding revenue sources.

Investment Story: From Transformation to Execution

Investors buy Honeywell for its ability to lead digital transformation in critical infrastructure.

The LS Electric partnership reinforces that position, but big structural changes still shape the outlook.

Honeywell’s upcoming three-way split remains the key short-term story driving investor sentiment.

Separation costs and execution risks could limit near-term upside despite long-term opportunity.

Connecting the Dots: Solstice Spinoff and Strategic Clarity

Honeywell also filed for the spinoff of Solstice Advanced Materials.

Both moves aim to sharpen focus and unlock value in high-growth markets.

Together, they signal Honeywell’s intent to build strong, specialized businesses for the future.

However, investors must weigh near-term costs against long-term structural rewards.

Long-Term Growth Forecast

Honeywell expects $45.8 billion in revenue and $7.5 billion in earnings by 2028.

That means a steady 4.6% annual growth rate and solid margin improvement.

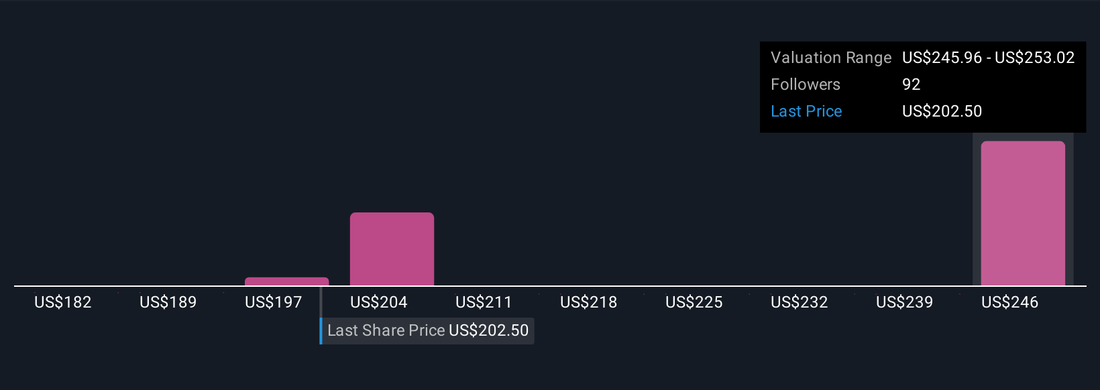

Analysts see a fair value of around $252.97 per share, roughly a 25% upside.

Still, others remain cautious, citing tariffs and separation costs that could slow progress.

Investor Takeaway

Honeywell’s energy and automation integration strengthens its long-term case.

But investors must stay alert as the company transitions into three focused entities.

Those who believe in Honeywell’s digital and energy strategy may find value in its evolution.

The LS Electric collaboration could become a key pillar of that growth story.