A Strategic Pivot

Emerson Electric is a leader in industrial automation. Its recent changes are attracting investors. The company reports its Q3 2025 earnings on August 6. Emerson's strategy is paying off. It is expanding in key regions. It is also successfully integrating software acquisitions. This is a good opportunity for investors. Emerson is ready for the industrial digitization boom. Its momentum and valuation metrics are aligned.

Acquisitions Drive Growth

Emerson acquired AspenTech in 2025. This was a major strategic shift. It moved from hardware to software solutions. Emerson also bought National Instruments and Afag. These acquisitions boost test automation and factory systems. They also improve AI-driven asset optimization. The AspenTech deal is especially impactful. The Control Systems & Software segment's EBITA margin is now 35%. It was only 14.8% a year ago. Analysts expect this segment's revenue to increase 7.5%. This brings it to $1.50 billion.

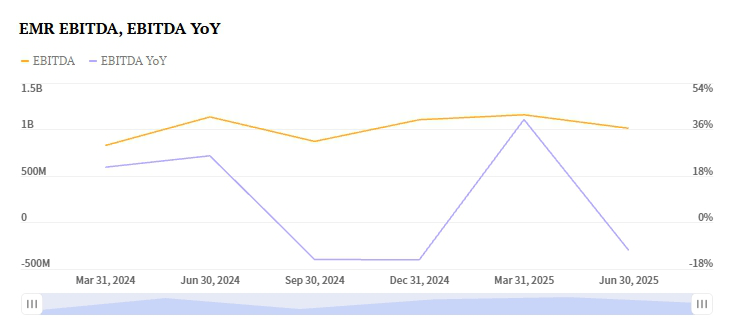

Emerson's 2024 performance shows the impact. Revenue grew 15.34% to $17.49 billion. The gross profit margin expanded to 50.79%. Operating cash flow was strong at $3.33 billion. Free cash flow was $2.91 billion. The company returned $2.3 billion to shareholders. Its balance sheet is manageable. Net debt is $4.61 billion. The debt-to-equity ratio is 0.77x.

Global Expansion Fuels Performance

Emerson's Q3 2025 earnings look promising. Strong growth is happening in Asia and the Middle East. Africa is also a key growth area. The Intelligent Devices segment is growing. It should see a 3.4% revenue increase. This brings it to $3.10 billion. Demand in battery manufacturing and energy projects drives this. E&C projects in South America are also strong. These regions offset softer demand elsewhere. Western Europe and North America are facing challenges.

Emerson's approach differs from its competitors. Schneider Electric saw a 5.9% decline. Its industrial automation segment struggled. The decline was in Western Europe and Asia-Pacific. Emerson's geographic flexibility gives it an edge. It focuses on high-growth markets.

Strong Earnings Outlook

Emerson's Q3 2025 earnings outlook is positive. Its Zacks Earnings ESP is +0.46%. This suggests it will beat the consensus. The consensus estimate is $1.51 per share. Emerson has a history of beating estimates. It exceeded them in the last four quarters. This includes a 0.4% surprise in Q2 2025. The company's Zacks Rank is #3 (Hold). This suggests a neutral short-term outlook. However, the positive ESP and cash flow are encouraging.

Competitors show mixed signals. Rockwell Automation's Q3 EPS is $2.69. It has a Zacks Rank of #3. Its Earnings ESP is +1.66%. But Rockwell faces margin pressures. Honeywell's EPS forecast is $2.64. Its Earnings ESP is +0.58%. However, its Industrial Automation division is slowing. Revenue could decline 5.7%. Emerson's superior margin expansion sets it apart. Its focus on software gives it an advantage.

Valuation and Future Potential

Emerson’s forward P/E ratio is projected to decline. It will go from 25.26x to 17.43x by 2028. This reflects normalizing valuation. Earnings growth is expected to accelerate. The company's target market is large. Industrial digitization is a $150 billion market. Emerson aims for 5-7% annual growth. It uses AI and digital twin technology. The AspenTech acquisition will generate synergies. Analysts project $200 million in annual synergies by 2027.

The stock has shown recent volatility. EMR closed at $141.40 recently. This was a -2.83% intraday change. Market expectations, however, remain bullish. Emerson is focused on reducing its debt. It targets a net debt-to-EBITDA ratio of 2.5x. This is targeted by 2026. Emerson is a leader in industrial AI. This makes it a strong case for investors.

Investment Thesis

Emerson Electric is a strategic buy opportunity. Investors must navigate short-term costs and currency headwinds. The company's momentum is strong. High-margin software acquisitions drive this. Regional diversification is also key. This positions it to outperform its peers. Risks like activist pressure exist. Market cyclicality is another risk. However, Emerson's cash flow is strong. Its margins are expanding. Its alignment with the industrial digitization trend is clear.

Conservative investors might hold the stock. The Zacks Rank is #3 (Hold). Yet, the positive Earnings ESP is a factor. Historical outperformance also supports a bullish view. Emerson continues to realize synergies. It is also deleveraging its balance sheet. The stock's valuation will reflect this transformation. It is moving from hardware to software. Its Q3 2025 earnings could be a turning point. It shows the company's new value proposition. Emerson is now a leader in industrial AI.